“Apple Card is an easy, intuitive way to expand your use of tap-to-pay and keep track of your spending.”

- Innovative app

- Beautiful titanium card

- Great customer service by text

- Accepts a wide range of credit scores

- iPhone only

- Cashback rewards are just ok

“Why you can trust Digital Trends – We have a 20-year history of testing, reviewing, and rating products, services and apps to help you make a sound buying decision. Find out more about how we test and score products.“

Mobile payment adoption in the U.S. is weak. While nearly two-thirds of Chinese consumers prefer to use mobile payments, just 8% of Americans do. Americans need a reason and incentive to adopt, and Apple believes the Apple Card is one way to do it.

The credit card — which relies on a partnership with Goldman Sachs as the issuing bank — focuses on an instant cashback reward system. With Apple Card, any transactions with Apple — in-store, online, the iPhone Upgrade Program, and even App Store purchases — all earn you 3% cashback. At select merchants, you now get 3% too, with more added all the time. Any other Apple Pay transaction nets you 2%, and if you use the physical titanium card, you get 1% cashback off each purchase.

You don’t need the best credit score

Applying for the card is simple, and available through the Apple Wallet app. Tapping the plus icon in the Wallet app adds the option to apply for the card. Apple asks you to confirm your name and address, verify your identity, and enter the last four digits of your Social Security number, as well as your income. That’s it.

The Apple Card’s application does not require a credit pull.

The Apple Card’s application does not require a credit pull. After completing the short one-minute application, you get an offer or a denial. Goldman Sachs only pulls your credit report when you accept the offer, something no other credit card does.

Don’t be scared to apply if your credit isn’t the best. Even with a low 600s credit score, I was approved due to two-plus years of flawless payment history, average utilization, and aging collections. I only got a $750 credit line and an interest rate of 23.99%, though, which barely allows me to buy the iPhone XR. Better credit profiles should see a 12.99 or 17.99% interest rate and a much higher credit line.

The beauty is how all of this happens through an app on your iPhone. A lot of the information it asks for may be pulled from your Apple ID, so all it requires are very few taps on glass.

Features? In a credit card?

Once you accept the offer, the Apple Card automatically adds itself to your Wallet. You don’t have to get the titanium card, but you should because Apple Pay isn’t accepted everywhere. Holding the card is something to behold, especially if you’ve never held a metal card before. It’s a hair thicker than average credit cards, and as meticulously designed as any other Apple product.

The Apple logo is etched into the upper left-hand corner of the matte white card, with Goldman Sachs and MasterCard logos on the back. Other than the magnetic stripe, you’ll only see your name.

Why? For security. Your credit card number lives securely within the Wallet app, away from prying eyes, and you can request a new number if you think it was compromised. The physical card is lockable within the Wallet app — it has a fixed card number different from the one in the app — and if it’s lost or compromised, you can order a new card. If you want to pay for items on the web with your card, you can request a virtual card number from the app, so your real one is never disclosed. It’s a big step for card security.

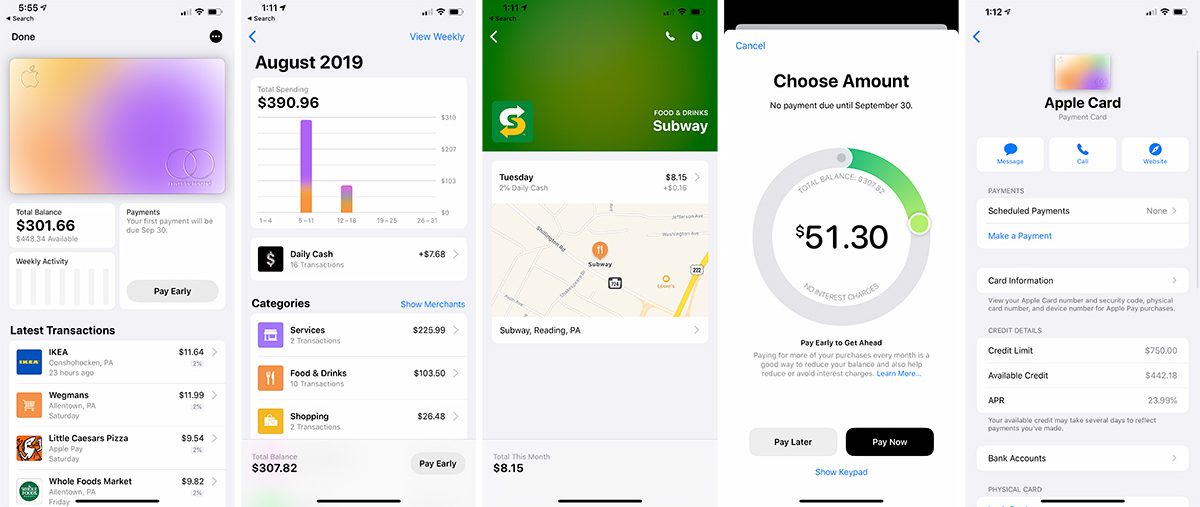

All your card functionality lives within the Wallet app. Tapping the card brings up a well-designed dashboard that exemplifies Apple’s knack for useful user interfaces. Your card, white at first like the physical card, changes colors based on the categories you use it for, like food or clothing. Below this is your current balance, a small graph of your spending, and a button to make payments.

Need to dispute a transaction? Report it right here within the app.

Like any other credit or debit cards in Apple Pay, recent transactions are found below the card, with some key differences. Transactions with the physical card also appear, and clicking on specific transactions presents you with a map of the location of the purchase to help you verify that it’s you making the purchases. Need to dispute a transaction? Report it right here within the app. Apple uses machine learning and map data to figure out the store name if it’s not readily available, and when it can’t, it doesn’t try to make a guess — but you can still see the map.

Daily Cash is the highlight. Instead of getting a cashback bonus at the end of the statement period like some cards do, Apple deposits it onto your Apple Cash card daily. You can use the money on your Apple Cash card to pay down your balance if you wish, or transfer it to your checking account.

The real security features of this card are not physical; they’re virtual.

Customer support, available via text message, is terrific. The representatives are quick to respond and friendly. There’s no more waiting on hold to ask basic questions.

Cashback

Apple has structured its cashback offer to encourage you to use Apple Pay. The 1% cashback for using the card is paltry by rewards card standards to be sure, and even the 2% when using Apple Pay is fairly pedestrian. But when using the card for any Apple service, iPhone Upgrade Program payment, or within the Apple Store, you’ll get 3%.

That 3% cash back race is expanding to other companies, too. Shortly after launch, Uber partnered with Apple to give users 3% on rides or Uber Eats purchases. T-Mobile purchases now offer you the higher cashback rate, as well as purchases at Walgreens and it’s Duane Reade locations. From our understanding, Apple intends to add additional merchants over time. Depending on your shopping habits, the higher rates at these locations could make the Apple Card a more attractive option.

Until the higher 3% cashback rate extends to more merchants, others cards offer better rewards.

At least for myself, this is beneficial. I have a T-Mobile phone, so I’d benefit from the higher cashback rate, and I do frequent Walgreens (and Duane Reades when I’m in New York).

This said, until the higher 3% cashback rate extends to more merchants, others cards offer better rewards. A few examples include the Chase Freedom (5% on select categories for a limited time every quarter), Capital One’s Savor (up to 4%) and Citi’s Double Cash (2% cashback everywhere). All of these might offer better average cashback rates depending on your shopping habits.

Privacy and Security

The real security features of this card are not physical; they’re virtual. Apple creates a unique device number for each Apple Card, kept within your iPhone’s Secure Element. To make a purchase, you’ll need both this number and a random security code generated at the time you tap.

Transaction summaries live on the device, so Apple doesn’t know what you’re buying. While Goldman Sachs will have access to this data to operate your card (for legal purposes), Apple has forbidden it to sell this data to third parties for advertising purposes.

And as we mentioned previously, you can generate new card numbers right from the app. There’s no need to wait for a new card when your card is compromised.

Better yet, you can chat with Apple Card support right from the app if you need to, meaning there’s no need to wait on the line for a robot to answer.

Using (and Paying on) the Card

Using the card is easy. Your card is usable through Apple Pay either as tap-to-pay or in Apple Pay-enabled apps immediately after approval. Once you receive the physical card, you can use it just like any other credit card. I was worried that inserting it into or swiping it through a reader might scuff up the card’s finish: so far, that hasn’t happened (I’ve used Apple Pay way more than the card, though).

Paying back your card is where Apple Card shines, and it’s completely different from any other card. Unlike other credit cards that want you to pay interest (and in turn make them money), Apple pushes you to pay more than your minimum payment, limiting interest.

The circular interface to make payments won’t be foreign to long-time Apple fans: it’s reminiscent of the navigation wheel found on early iPods. It shows how much Apple recommends I pay, and also shows how much interest I will accrue if I choose to pay less. Whatever payment you make, it’s automatically reflected in your available credit, and the money was withdrawn from my account the following morning. Who knew paying a credit card could be this pleasant

I’ve found that on average, I’m paying off my balance on this card much faster than others. I think this is a result of the interface. If Apple thinks you’re not paying enough the payment circle turns red. A payment that significantly reduces your interest but doesn’t avoid interest on your next statement turns it yellow, and payments that prevent any interest turns it green.

That little visual nudge gives you an extra push to pay more, and so far, I’ve been able to avoid interest charges. I might not have such luck this month. No worries, though. I’ve accumulated enough Apple Cash rewards to remain in the plus for quite awhile.

Our take

The Apple Card is improving with time, and will spur you to use tap-to-pay quite a bit more. However, even with the addition of new partner retailers offering 3% cashback, there are better rewards cards out there. The card’s appeal is its ease of use and rewards on Apple products, not a broad cashback bonus.

Is there a better alternative?

Yes, if you have excellent credit. As I’ve mentioned throughout this review, many credit cards that focus on cashback rewards will offer better rates at more retailers. However, cards with excellent rewards require a high credit score, so they’re not accessible to everyone.

Will it last?

Of course. It’s a credit card.

I’ve read reports of the cards discoloring when coming into contact with the leather in your wallet or denim. It’s bizarre that Apple didn’t test out the card’s durability with what’s probably the two most common materials the card would come in contact with, but this is a minor concern.

Should you get it?

Yes. The Apple Card is a solid pick if you want a card that prioritizes an intuitive interface, ease of use, and good customer service.