- Home

- Social Media

Social Media

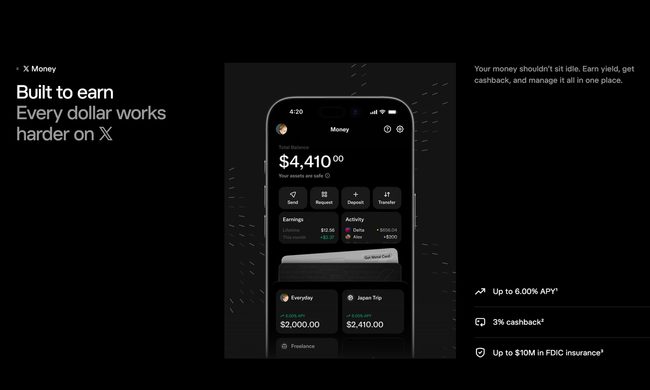

X Money is finally here, and it’s much more than a digital wallet

X Money has officially launched in the US, bringing peer-to-peer payments, a Visa debit card, and high-yield savings accounts to eligible X Premium users.

Europe plans a wide social media ban for children

A panel of experts has recommended that the European Union bar children under 13 from social media, with looser rules for teens up to 18.

The days of unrestricted social media for children may be coming to an end

Governments worldwide are introducing or considering social media bans for children, as concerns over mental health, online safety, and addictive algorithms continue to reshape digital policy.

Meta just pulled its most controversial AI image generation feature days after launch

Meta pulled an AI image generation feature that let users create images from any public Instagram account by default.

Your YouTube playlists can now become actual TV shows, but there’s a catch you need to know

YouTube Partner Program creators can now organize videos into episodic shows with seasons, serial or non-serial structure, and custom artwork.

I knew there was plenty of AI slop on LinkedIn. Shocking report says the problem is far worse than suspected

LinkedIn supplied almost two-thirds of the AI-generated social content flagged in a million-post analysis, despite representing only one-third of the material scanned.

Your phone is not trying to poison your water, but influencers found a $50 fix anyway

Influencers are selling $50 EMF straws as protection from everyday electronics, but the evidence is thin and the real product may be tech anxiety dressed as wellness.

X could soon alert you when a post you liked or reposted gets fact-checked

X is working on a new feature to notify users directly when a post they liked, replied to, or reposted gets a Community Note.

Meta’s new AI can generate images of you from your Instagram, and you’re opted in

Meta's Muse Image lets anyone use your public Instagram photos to generate AI images of your likeness, without notifying you, and it's switched on by default.

Meta’s new image and video AI tools let you turn Instagram into your creative mood board

Meta's Muse Image is live now on meta.ai, Instagram, and WhatsApp with agentic image generation, and Instagram-handle prompting.

Social media ban for young users is proving to be an age verification nightmare

Researchers created 50 social media accounts claiming to belong to 16-year-olds and found that none of the major platforms asked users to prove their age

X wants to keep your video edits in-house, and it’s starting with captions and custom backgrounds

X has rolled out a redesigned Video Editor and Recorder for iOS, adding multilingual captions and a green screen tool so creators can edit their videos without leaving the app.

Reddit’s AI is hunting brands that dress marketing slop up as honest opinions

Reddit is deploying large language models against brands and marketers planting fake conversations that could later surface as trusted recommendations in ChatGPT and Gemini.

AI tools can quietly shift your opinions when they “clean up” your social media posts, study finds

A new study found AI tools consistently nudge social media posts toward one side of a debate, even when told to preserve the meaning.

I spend hours on YouTube Shorts, and these are the features I now can’t live without

I use YouTube Shorts more than I'd like to admit, and these new features have genuinely changed the way I watch. Chances are, you'll appreciate them too.

As AI turbocharges digital abuse, UK agencies urge parents to limit who sees kids’ photos online

The UK's NCA and IWF are urging parents to tighten social media privacy settings as AI tools make it easier to turn ordinary images into abuse material.

Google Maps could soon order food for you using Gemini

Google Maps is reportedly developing a Gemini-powered feature that could let users discover restaurants and place food orders without leaving the app.

Most Americans want kids off social media before 16, new survey shows

A new Pew Research Center survey has found that 56 percent of Americans support banning social media for anyone under 16, with support crossing party lines and age groups.

Meta under scrutiny after Instagram approved child abuse advertisements in India

Instagram approved and displayed advertisements promoting child sexual abuse material in India before removing them following an investigation.

WhatsApp pausing usernames for hundreds of millions of users over fraud fears

WhatsApp’s username feature has run into trouble in India, where officials are concerned about impersonation fraud and fake accounts.

X wants you to go live with its new streaming hub, and is offering $1 million to make it worth your while

X has launched Live Studio, a dedicated streaming command center inside Creator Studio, and is putting $1 million on the table to incentivize creators to go live on the platform.

Reddit is ending anonymous browsing on old Reddit, and longtime users are not happy

Reddit is locking down old.reddit.com with a login wall, and the admin's post hinting it may not last forever has longtime users worried.

TikTok, Instagram, Snapchat, and YouTube are failing kids with broken safety features, research finds

A new study tested 86 child safety features across TikTok, Instagram, Snapchat, and YouTube, and found that more than half were broken, buried, or missing entirely.

Yet another research proves TikTok injury advice is just downright bad

A new study found TikTok videos about ACL rehab exercises were poor overall, raising fresh concerns about teens using viral clips for injury recovery advice.

Instagram is testing a more convenient way to tune recommendations

Instagram is testing new shortcuts for Your Algorithm, making it easier for users to adjust recommendations while browsing Feed and Reels.

Snapchat Planets Meaning: Order, Rankings, and How Friend Solar System Works

Snapchat Planets turns your friendship ranking into a tiny social solar system, where being Mercury is elite and Neptune might sting a little.

Instagram lands on Samsung TVs, with episodic series and live TV coming to your screen soon

Meta is testing interest-based channels, phone-to-TV casting, and a horizontal video hub as Instagram for TV expands beyond Samsung's launch.

Social Media News

Social Media Guides

Social Media Features